I’ve been thinking about currency devaluations lately so I thought that I should take a look at the most talked-about recent case of currency devaluation, the Icelandic Krona, along with its effects on the Icelandic economy.

Here’s a chart of the Krona vs. the EUR and the USD.

|

| source: Central Bank of Iceland |

As the chart makes obvious, the Krona was devalued enormously during 2008. Popular wisdom wants currency devaluations to be expansionary, but actually literature on the subject is mixed about that. I just want us to wonder if there is such a thing as a free lunch. If currency devaluations were that beneficiary with no strings attached then everyone would choose to follow that route, wouldn’t they?

Before expanding on the subject I want to say something. A common comparison that a lot of commentators draw on is between Ireland and Iceland. I think that this comparison is simply wrong, since we are talking about two economies with totally different fundamentals that just happened to be plagued by two common malaises, a property bubble and an oversized banking sector with risk-heavy balance sheets. That’s not enough to make them quite the same, is it? But for the sake of argument I’m going to include Ireland in some of the charts since I think that even these arguments are overplayed. I will explain what I mean by different fundamentals later on.

First of all let’s see how Iceland fared growth-wise. Here is a chart of Iceland’s real GDP growth.

|

| source: Eurostat |

Iceland devalued during 2008 but recorded positive real GDP growth only in 2011. A good question is what happened then. We’ll answer that later.

The reason why the currency devaluation by itself was not adequate for Iceland to get back on the growth wagon is probably that Iceland’s external sector was not big enough to bear the growth burden by itself and that the recessionary forces were too strong (exorbitant external debt played a role too).

|

| source: AMECO, own calculations |

Everybody’s first thought when hearing about currency devaluations is exports. Here is Iceland’s exports chart.

|

| source: Eurostat |

The year that the Krona devaluation took place, 2008, exports spiked significantly but this was mostly due to increased aluminum exports, a trend already in place for some time. This has nothing to do with the devaluation since it is associated with large scale investments in the aluminum sector launched in 2003. Besides aluminum, capital goods contributed significantly to total export growth in 2008 but stagnated after that.

The J-curve effect states that any positive effects from the currency devaluation on exports materialize with a time lag, at least that’s what happens in most cases. The J-Curve effect also states that before exports start growing, a brief slump might be recorded. Maybe that can explain the slump in Q4 2008. In 2009 exports grew by 7,2% in real terms according to Eurostat’s data but according to actual quantity data from Statistics Iceland, exports were mostly flat (as you can see in the chart below). In 2010 export growth in real terms eased even more, while it was stagnant in actual quantity terms.

Most product classifications didn’t grow at all post-devaluation and many even declined quantity-wise. Here’s a chart about the major contributors to export growth (again quantity-wise) the years in question.

|

| source: Statistics Iceland |

All in all, if my ramblings above are correct, the Krona devaluation didn’t help Icelandic exports as much as it is heralded (always in actual quantity terms) and the adjustment that took the country’s trade balance into surplus territory originated mostly from the import-side (i.e. decrease in imports). Moreover, I think that Iceland was “unlucky” that the first year, after the devaluation took place, coincided with the worst (or is that the only?) slump in international trade in the past few years.

|

| source: Statistics Iceland |

One more thing that was talked about extensively in the economic press or wherever else, is that the devaluation option was not that painful. Well, I will put on a few more chart (hope you are not asleep by now) so that you can reach your own conclusions.

Here’s real private final consumption expenditure for Iceland.

|

| source: Eurostat |

Does that monumental decline in real private final consumption expenditure seem painless to you? Also this is the answer to the question that I posed in the beginning of the post about what happened and Iceland started growing in 2011. Private consumption expenditure started growing, that’s what happened.

To give you a clearer picture, here are Iceland’s real imports.

|

| source: Eurostat |

The time that monstrous declines in real imports started being recorded, maybe can help us in the task of timing when the effects of the devaluation started kicking in. That time is Q4 2008, like we had speculated above.

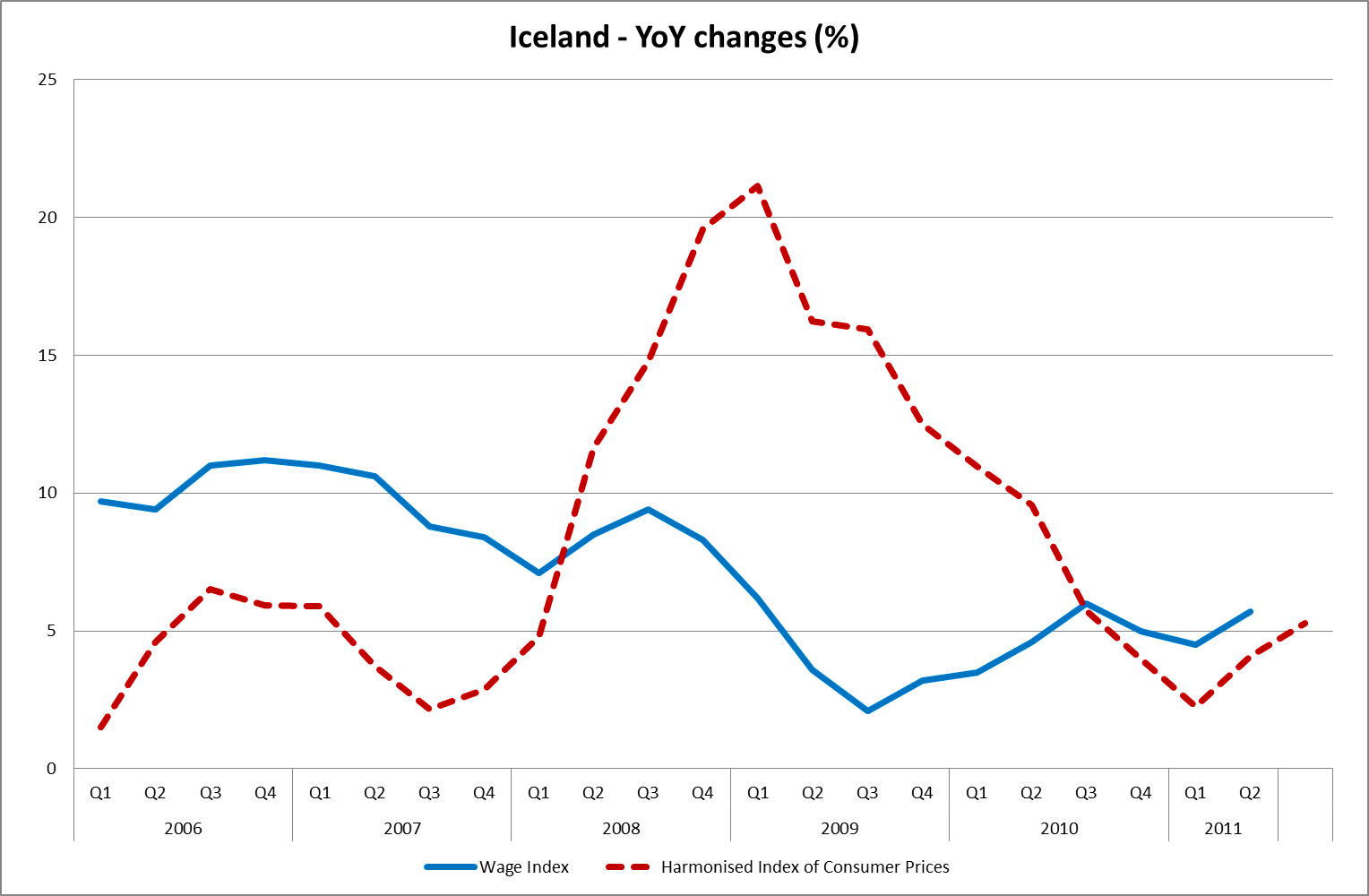

Of course, private consumption didn’t start growing out of the blue in 2011. The main catalyst was that real wages started growing. Since private consumption was heavily depressed during the previous couple of years, it could that some low-base effects are at work here too, but only time will show what is what.

|

| source: Statistics Iceland, own calculations |

One last thing. One of the problems associated with currency devaluations is that the country “imports inflation”. The prices of inputs rise and if that is transformed to an inflation-wages spiral then any devaluation-induced cost advantage could be wiped out shortly. One-off devaluations don’t have that effect usually but continuous devaluations tend to do just that.

What that means is that for devaluations to be effective real wage growth has to remain subdued, which again means pain for people. Another option exists and that is keeping the exchange rate depressed through the accumulation of foreign reserves, but that contributes in keeping private consumption weak as well. In my humble opinion for a devaluation to have a lasting effect on growth and exports, countries that choose to follow that strategy must work hard to increase investment or if that’s not possible then to attract foreign direct investment (FDI), or even both. Last but not least for any devaluation gains to be long-lasting the country has to adress any structural problems it has.

Currency devaluations are not as suitable for all countries. Countries with a large external sector that one-off factors had contributed to its current-account being in the red for a few years, could relatively less painfully, adjust through currency devaluation. Countries with chronic competitiveness problems and miniscule external sectors could find that currency devaluations are extremely painful. This is just one policy path that could help the current account swing into surplus, as is internal devaluation. Both of them though involve severe economic and social pain…

P.S.1. Since I don’t have any special knowledge about Iceland all these could be simply wrong, so if anybody that possesses more knowledge on the subject thinks that I don’t know what I’m talking about, please say so in the comments section and enlighten me about the actual situation.

P.S.2. I mentioned Ireland's fundamentals, here is the relevant chart. One look at it makes obvious what I meant by different fundamentals.

|

| source: AMECO, own calculations |

No comments:

Post a Comment