I know that I’ve written excessively about labour productivity. Perhaps I’ve done so to such a degree that I could rename the blog “Labour Productivity Tragedy” and the name would not look out of place. Bear with me though, since I think that today’s post angle is just a tiny bit interesting since the whole matter is looked at through the lens of a certain structural feature of the Greek economy.

Unfortunately, the data points of today’s post are a bit dated, since they are derived from a couple of rather focused Eurostat surveys/projects. I’m sure that this doesn’t make them any less valid, since things are not likely to have changed in such a dramatic way in the intervening years.

First, the so called structural feature of the Greek economy. It is widely known from word of mouth or anecdotal evidence that the bulk of Greek firms are rather small and mostly fall into the SMEs category. Here is some official Eurostat numbers circa 2007.

|

| source: Eurostat |

To delve a bit deeper we can say that Greece has the highest % of micro enterprises (1-9 employees) in the EU, the second lowest % of small enterprises (10-49 employees), the lowest % of medium enterprises (50 – 249 employees) and again the lowest % of large enterprises (over 250 employees).

In order not make your eyes bleed from too many graphs I will only put on the relevant graphs for micro and large enterprises.

|

| source: Eurostat |

|

| source: Eurostat |

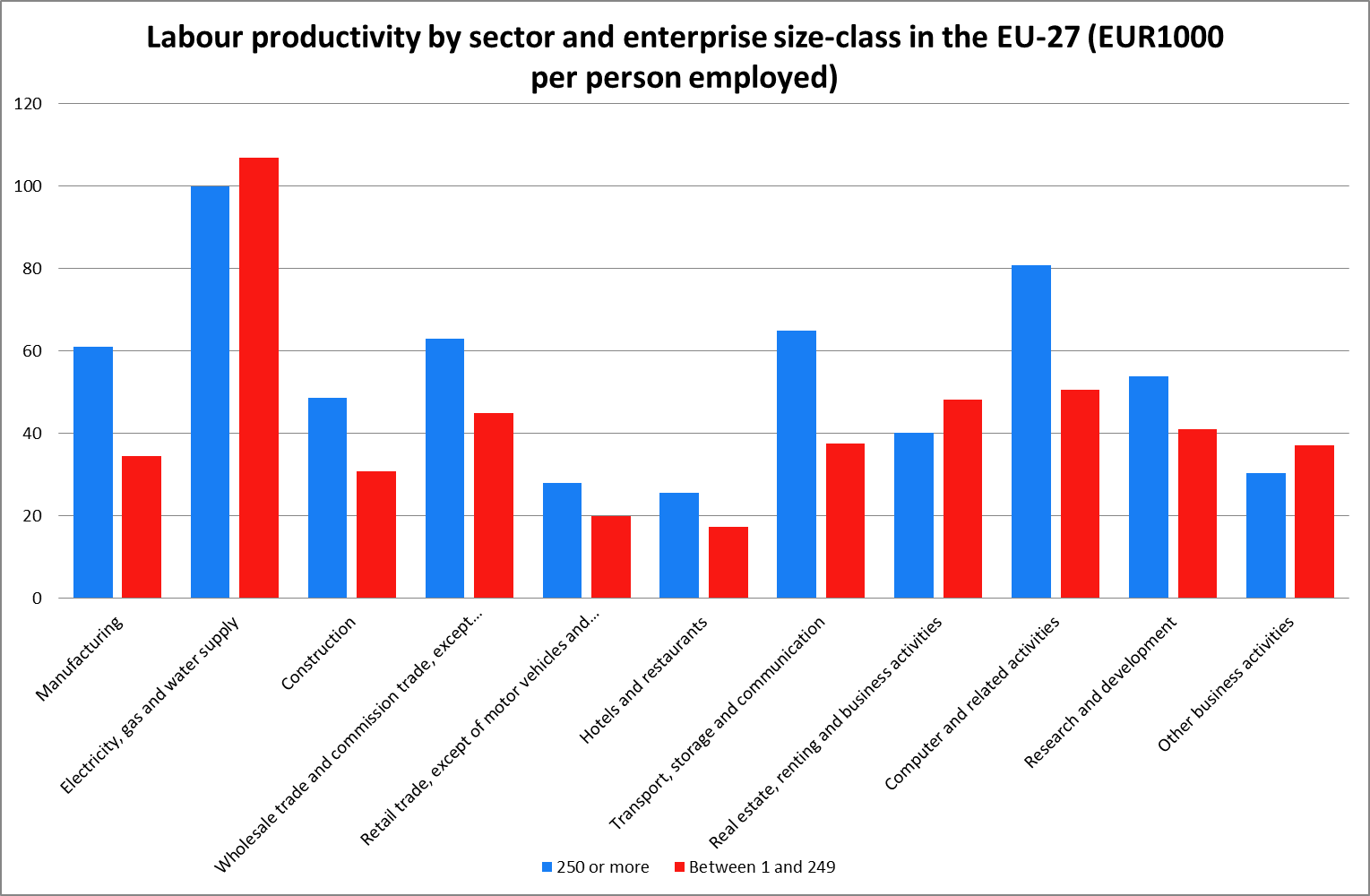

Based on another Eurostat survey, circa 2005, for most sectors labour productivity increases in line with the firm’s size (measured by the number of employees). There is a newer survey for 2007 (with some individual sector figures dating back to 2006) but I’ve chosen to use this one because it has an aggregate productivity figure for manufacturing.

|

| source: Eurostat |

In the chart above I’ve plotted labour productivity for micro, very small, and small enterprises. The relevant figure for utilities is obviously an outlier and it makes the other labour productivity differentials seem trivial but I’ve plotted the differentials in another chart later on.

Here’s the chart for medium and large enterprises.

|

| source: Eurostat |

And here’s the chart showing productivity differentials among firms of different size classes.

|

| source: Eurostat |

For the vast majority of the sectors pictured in the charts, labour productivity increases in accordance with the firm’s size. I can point out two notable exceptions; utilities and other business activities. For the first one, the implications for Greece due to its renewable energy sources potential are obvious. As far as the second one is concerned, no matter how hard I looked it up, I couldn’t find what it includes, if anyone has a clue please do enlighten me.

As you can notice with even a cursory glance at the second chart, all Mediterranean countries exhibit high % of micro enterprises. Could this (besides any regulatory, financing or other unique domestic issues) be attributed to the cultural features of the said countries? Or the temperamental features of the countries residents?