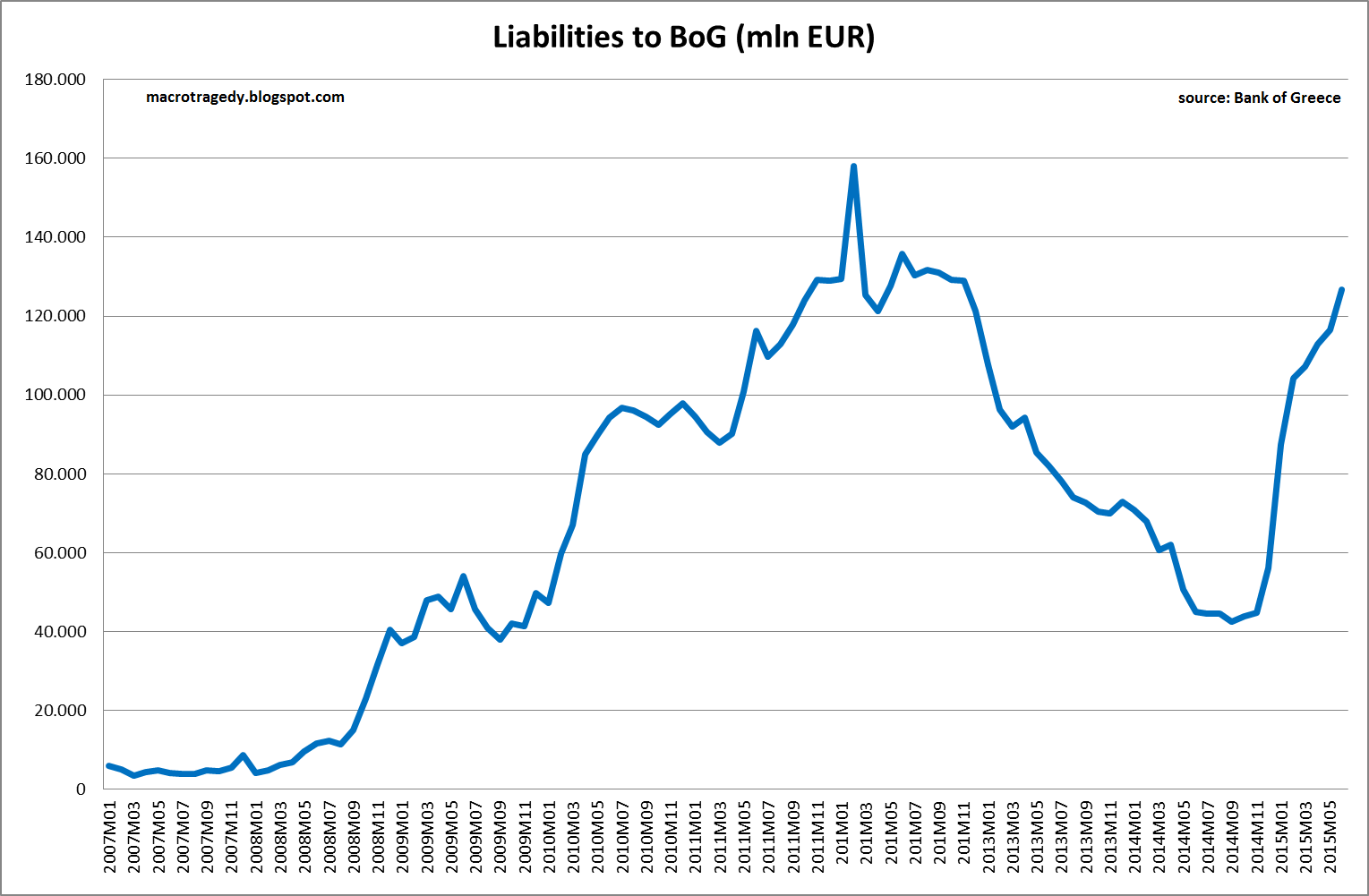

There's a lot of talk in Greece regarding the impact of capital controls on employment. Since employment data are published with a great lag (and an even greater one over here) one way to gauge their potential impact is through DG ECFIN's leading indicators.

Employment expectations indicators for Industry and Services surely paint a pretty dismal picture.

|

| source: DG ECFIN |

One could think that this doesn't carry much weight since it is just an expectations indicator and these are not immune to overreaction or survey participants' judgement errors. It would be informative to see how those indicators predictive powers have fared in the near past.

I turned DG ECFIN's survey data into quarterly by computing the quarterly averages in order to compare them with actual employment changes. Since constructing an composite employment measure for services would take some time I've just included industry data in the chart but these are more than enough in order to get a sense of things I think.

|

| source: DG ECFIN, Eurostat, own calculations |

The employment expectations indicator reacted a bit quick in 2009-2010 but actual employment changes eventually (and sadly) caught up with its "predictions". Of course, there is prior experience of how the said indicator reacts to the imposition of capital controls, in Cyprus.

|

| source: DG ECFIN, Eurostat, own calculations |

In Cyprus the said indicator had put in a bottom (as we can see ex-post) before the imposition of capital controls and their effect was a mere blip since the indicator rebounded the next month. Of course, the setting was quite different there, since this was right after election while over here we got elections coming up (yet again) next month. And these prolong, the already sky-high, uncertainty.

To wrap this up, only time will tell what capital controls' actual impact on employment will be. Yet things, ex-ante, are not looking that good. Let's hope that reality will prove these pessimistic omens to be false.