We hear a lot about the uneven recovery in the EU. Uneven since the core grows faster than the periphery.

Well, I happen to believe that recovery among core countries is uneven as well.

Here’s a chart about retail sales in Germany and the Netherlands. Does this match your definition of even?

|

| source: Statistics Netherlands, Statistisches Bundesamt Deutschland |

That’s what set me off to look further into it, since headline GDP figures seem good for both.

In the first quarter of 2011, Germany real growth rate stood at 4,8% while the same figure for Netherlands was 2,3%. Well, on the surface things for Netherlands look pretty robust, god knows what we Greeks would give so that we could have a real growth rate of 2,3% at the moment.

|

| source: Eurostat |

But under the surface things are not that rosy and the unevenness of the two countries recoveries starts to show. Here’s the culprit.

|

| source: Eurostat |

Final consumption in Germany grew by 1,9% in real terms, the highest Q1 growth rate Germany has seen since Q1 2001, while in the Netherlands final consumption grew by just 0,3% in real terms.Could this be pent-up demand? Is this sustainable? I wish I knew...

My guess is that the one factor that could largely be blamed for final consumption’s weakness in the Netherlands lies in the next chart.

|

| source: Eurostat |

Households in Netherlands are heavily indebted and doubled their leverage during 1995-2009, while German households’ leverage was essentially flat. The term balance sheet recession seems apt for Netherlands since households balance sheets are heavily burdened with debt (although the country is not a recession presently).

The vast majority of household debt should be in the form of mortgages. As I had pointed out in an older post the vast majority of mortgages in Holland seem to be fixed rate ones. That means that when interest rates are high and rising households still have to pay the same interest rate. But in a low-interest rate environment such the one that we’re living in now (although the ECB is doing its best to change that) the interest rates that households have to pay are not lowered meaning that their interest burden remains unchanged. This obviously affected final consumption adversely.

|

| source: Eurostat |

Let’s hop to the next one. Gross fixed capital formation was especially weak during the recovery for the Netherlands. It only turned marginally positive during Q4 2010 and it grew by an impressive 10% during Q1 2011 although when compared to a really low base in Q1 2010. That was a welcome positive contribution for Netherlands’ growth rate. On the contrary gross fixed capital formation was robust during the recovery for Germany.

|

| source: Eurostat |

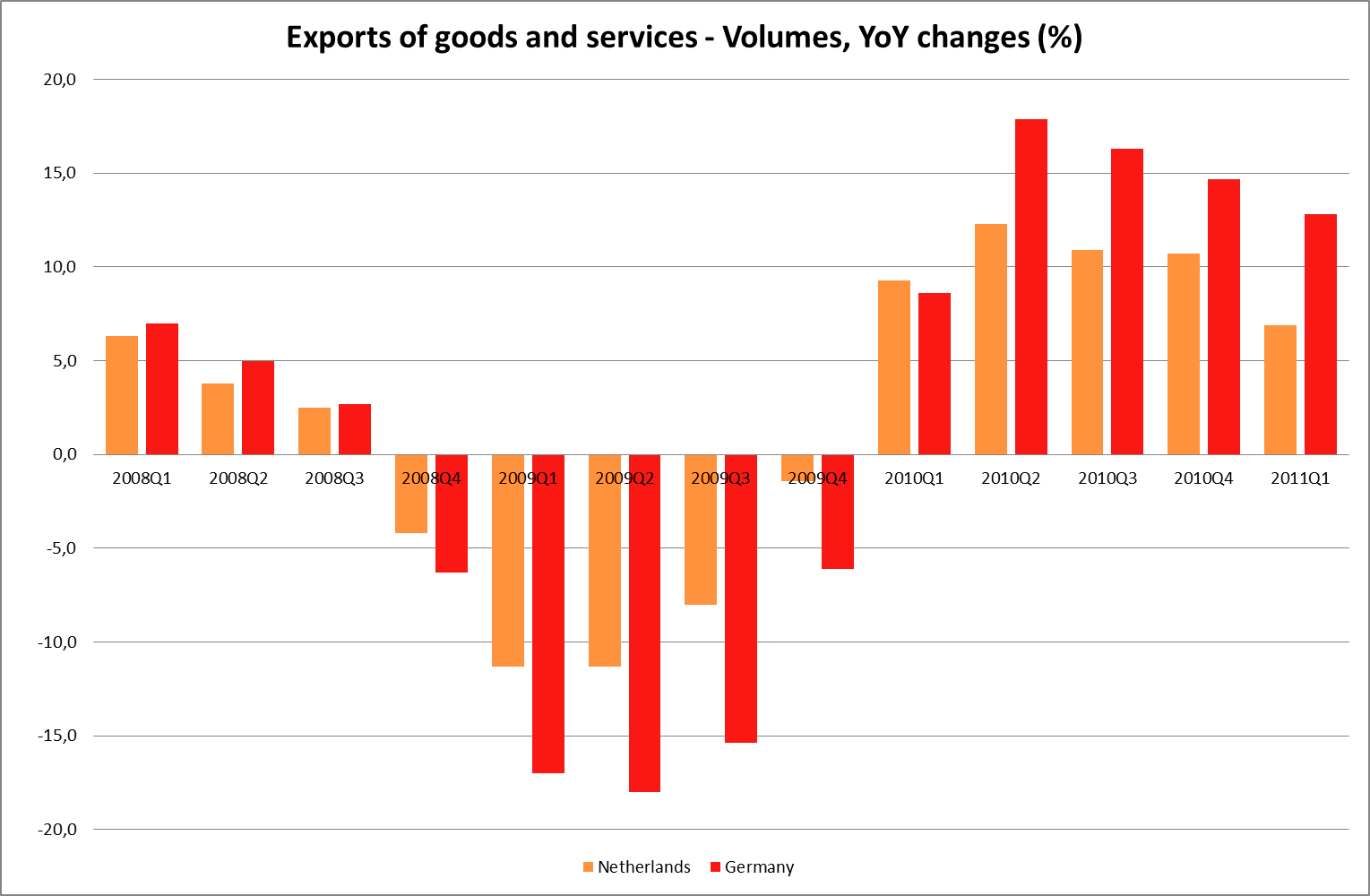

Let’s take a look at exports now. During the recovery, exports growth was especially strong for Holland and Germany alike, well, maybe German exports performed a bit better than Dutch ones.

In my humble opinion we are looking at the main reason behind Netherlands’ positive growth rate. If you think that a above 2% growth rate cannot be achieved through export growth mostly then maybe you have to keep in mind that Dutch exports amounted to 70,34% of GDP in 2010.

A good question is what part of this astronomical figure can be attributed to re-exports due to the importance of Rotterdam’s port. Well, I don’t know the answer to that, maybe a lot maybe a little; I somehow doubt that the answer could be none though.

|

| source: Eurostat |

Let’s have a peek at imports now. Since final consumption is so weak one would expect that import growth would be anemic as well but this is clearly not the case. By looking at the way imports and exports change over time I get the feeling that their correlation should be really high, which in my mind makes the scenario that re-exports comprise a large parts of exports all the more probable.

If that is so, a good question is what the actual growth rate of Netherlands is? Of course, I could be totally wrong about this since I’m only guessing and just looking at GDP components stats was never a good way to gauze whether something like that is true. Regardless of my speculation here it is true that Netherlands have a really dynamic export sector.

What is undeniably true though is that the touted recovery in uneven not only among the core and the EU periphery but among core countries as well. GDP growth in Netherlands appears to rely mostly on export growth, since final consumption seems to be weak. What happens if emerging markets slow? Of course this is a question not just for the Netherlands but also for Germany, since German consumers have proved to be particularly fast to retrench when things get ugly…

No comments:

Post a Comment