Anyone casting even a furtive glance at Greek macro data must have noticed that Greek manufacturing is currently staging a much needed bounce. A bounce that still belongs to the "too little too late" category if one compares its magnitude to that of the massive contraction that the sector underwent during the 2008 - 2012 period. Let's drill down a bit more and look at the specifics of this bounce and the underlying situation in individual sub-sectors.

|

| source: ELSTAT, own calculations |

In case someone wants some perpective, it should be remarked that the lowest the overall production index got was 30,3% off its highs and that the current bounce brings it 10,4% off its lows, i.e. it currently stands 23,1% off its late-2007 highs.

|

| source: Eurostat, own calculations |

I thought that it would be very interesting to see the overall index's moves de-composed into these of its main components (unfortunately the narrowest de-composistion ELSTAT offers, includes 24 sub-sectors and since I couldn't find a similar methodological explainer for Eurostat so I went for that) so I re-constructed the headline index from scratch. The resultant index wasn't an exact replica (for reasons that obviously elude me) of the original but it was decent enough I think. Anyway, here is how it stacks up compared to the real thing.

|

| source: ELSTAT, own calculations |

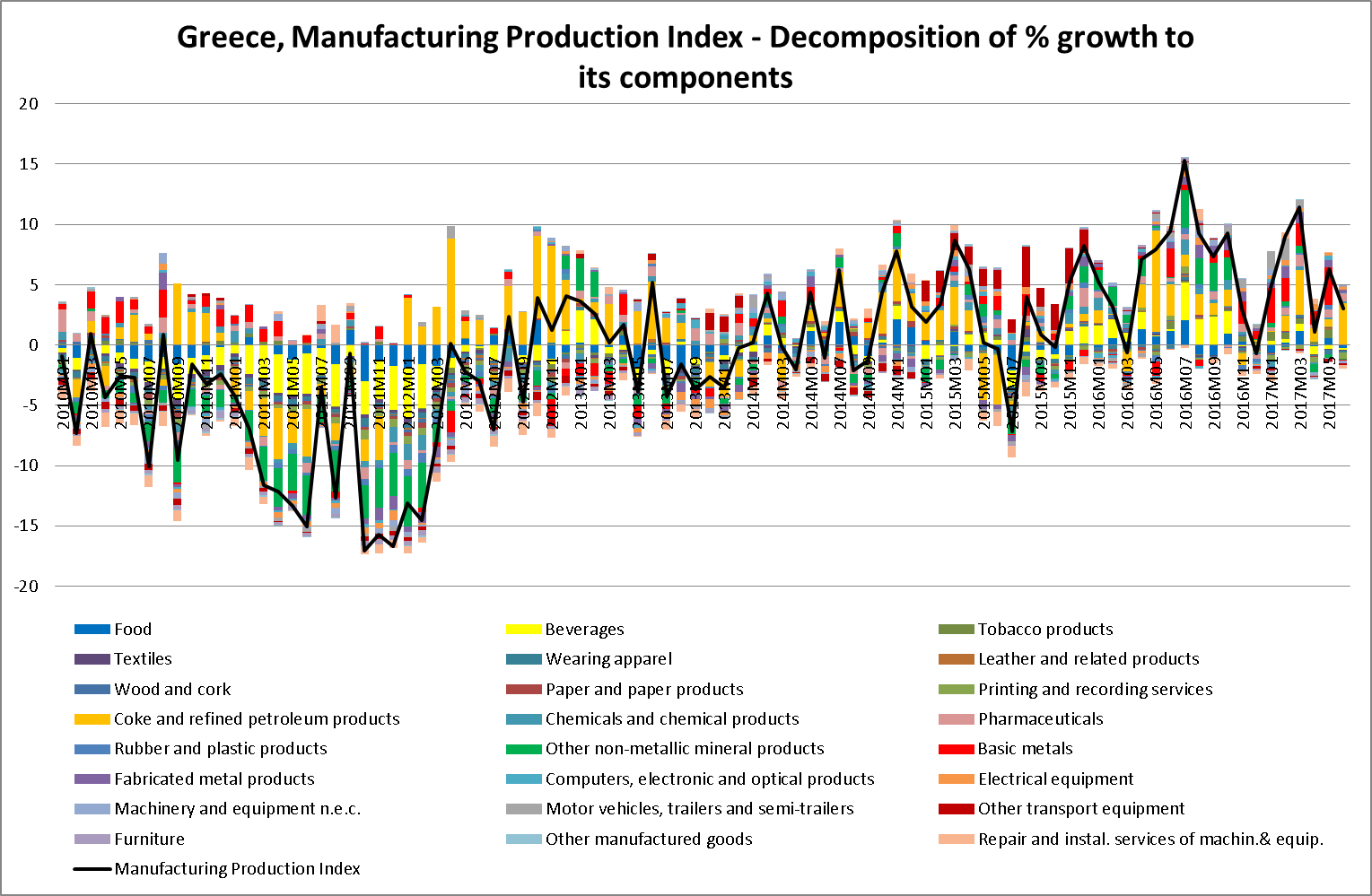

And here is the decomposition. I know one gets woozy by all the tiny coloured bars but I did my best to give somewhat flashier colours to the index's main components (i.e. Food ~ 19,87%, Oil Products ~ 15,08%, Basic Metals ~ 7%, Beverages ~ 8%, Non-metallic Minerals ~ 8% of total).

|

| source: ELSTAT, own calculations |

The current rebound's catalysts are mostly oil products, basic metals and pharmaceuticals while beverages and non-metallic minerals contributed too to the previous big production spike in mid-2016.

Headline figures show that momentum is currently waning but this could very well be due to one or two big sectors slowing while, beneath the hood, growth remains broad-based and buyoant. One way to see if this is the case here is to count the sub-sectors that are currently in expansion mode.

|

| source: ELSTAT, own calculations |

It seems that, below the hood too, the rebound is indeed moderating since out of the 24 sub-sectors charted here, just 8 were expanding in July compared to a high of 21 in July 2016.

Taking a look at individual sub-sectors, it seems that the only one going through a phase of - seemingly - unhindered growth is pharmaceuticals whose production is climbing to new highs compared to all the other sectors that still try to reach their previous highs. What's more, secondary, mostly inward-oriented sectors, have been all but annihilated by the crisis, with their current production levels hovering at about 20% of their pre-crisis highs.

|

| source: ELSTAT, own calculations |

To wrap this up, the current rebound in Greek manufacturing is decent in magnitude but it currently appears to be slowing. It remains to be seen whether it will gain steam again of the current policy mix of over-taxation, high energy costs and cost-of-capital will make it succumb to the pressure.