Lots of

commentators claim that the deterioration in the Greek current account can be

blamed on the country adopting the Euro. Well, if you just look at aggregate

figures it may seem that way.

|

| source: Eurostat |

If one bothers to drill down a bit more then a

slightly different picture may start to emerge. Let’s take a closer look then.

One factor that contributed to the widening of

Greece’s current account deficit was the drying out of current transfers from

European Union after Greece’s accession in the EMU.

|

| source: Eurostat |

Next I would like to take a more detailed look

at the merchandise trade balance (according to the SITC classification).

The relevant balances for Food,Drinks&Tobacco

and Chemicals were essentially flat over the 1995-2011 period.

|

| source: Eurostat, own calculations |

Now let’s

take a more detailed look the individual balances that contributed to the

deterioration of the current account.

|

| source: Eurostat, own calculations |

Out of all the sub-accounts of the merchandise

trade balance the one having the biggest net contribution to the widening of

the current account deficit is the Mineral Fuels balance. I think it is obvious

that the deterioration of this balance have nothing to do with the

deteriorating competitiveness of the Greek economy per se, but its wide deficit

is due to structural factors and buoyant demand over the 00s.

The Machinery&Transport Equipment balance

deficit widened significantly during the run-up to Greece’s accession in the

EMU and then narrowed exhibiting

widening spurts which contributed in the periodical deteroration of the

overall deficit (like for example in the 2005-2008 period when Greece recorded

the widest current account deficit in the years that my data run). This occurrence

underlines one single fact, that the household consumption bubble that Greece

experienced in the 00s was the driving force behind the current account’s trajectory.

This was a demand-pull phenomenon. Investment in machinery and investment in

transport equipment were both quite robust in the 00s so the fact that the balance improved

simply means that GDP expanded more than said imports and that the driving

force was due to other factors (i.e. demand-driven).

I think that the next chart is

interesting in this respect.

|

| source: Eurostat, own calculations |

Our next stop is the Other Manufactured Goods

balance, which deteriorated as well. I would like to highlight a couple of

points. First, notice that the deterioration commenced before Euro membership was

a reality but nonetheless continued during the 00s. Second, during the

2005-2008 period when this particular balance recorded its highest deficit

these past 15 years, the Greek private consumption bubble reached its apogee, something

which in my humble opinion means that at least part of this deterioration was

again a demand-pull phenomenon. Undoubtedly, part of the widening of this

balance can be attributed to falling competitiveness. But what part of it is

due to the Euro’s strength and what part of it should be blamed on the

accession of the Central-eastern European (CEE) countries and the explosive growth

of their exports? I can’t apply econometrics to give you a

precise answer, but I can attempt to shed some light with the next few charts. We

shouldn’t forget that (at least in the start, since now CEE countries have

upgraded their export baskets while Greece has not) Greece’s basket of

merchandise exports was quite similar with that of certain CEE countries.

The next

chart can serve as further evidence of the validity of the claim that

households’ final consumption was the main catalyst behind the said balance’s

deterioration.

|

| source: Eurostat |

Of course,

correlation is not causation but this a rather close fit, don’t you think..? If

you believe that this would usually be the case, then take a look at the same

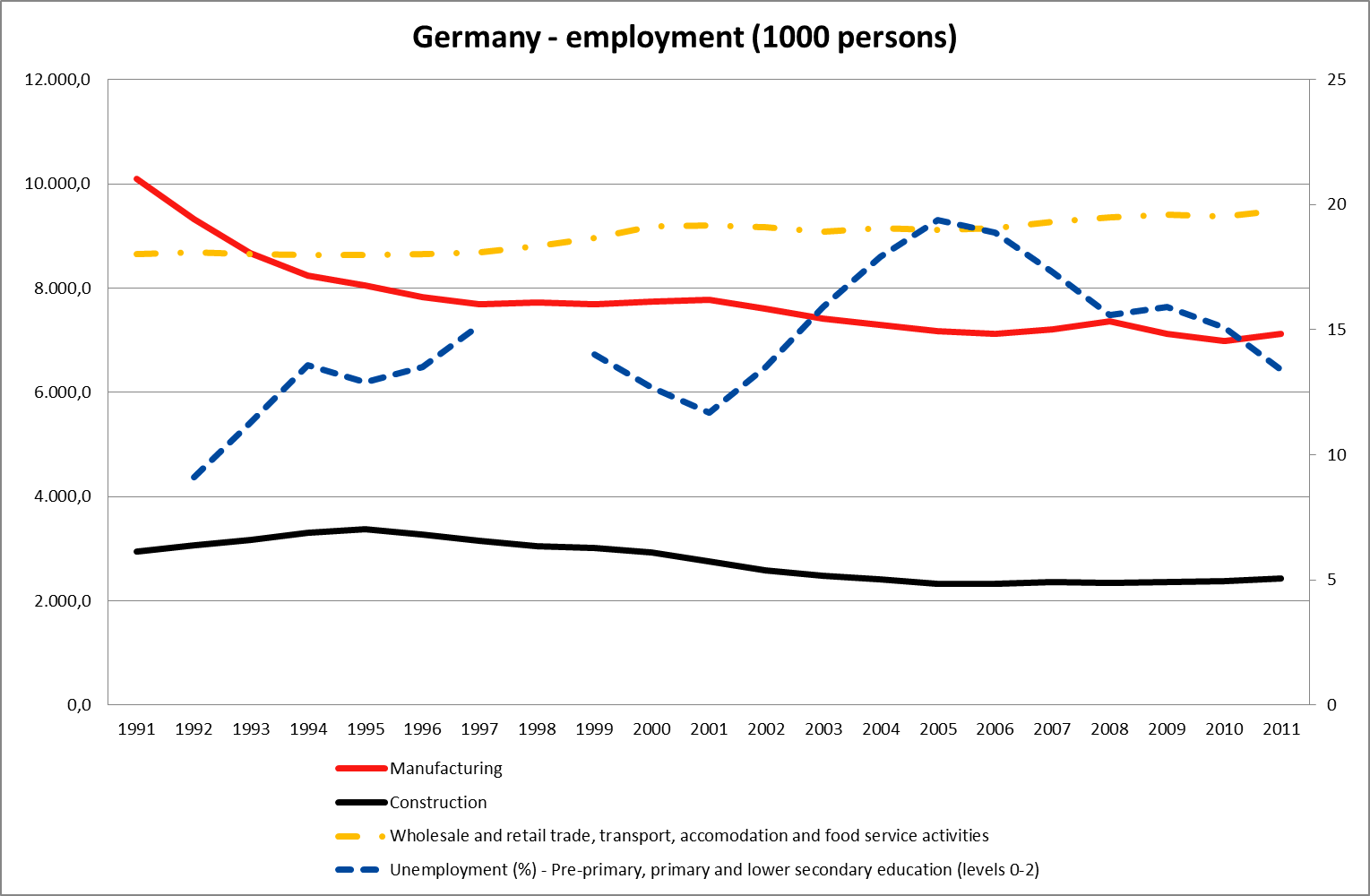

chart for Germany, that did not experience a households’ final consumption

bubble. Not such a good fit, is it?

|

| source: Eurostat, own calculations |

Now a simple observation. If the widening of

the merchandise trade deficit could be blamed on Greece’s loss of

competitiveness then Greece must have recorded significant losses in its market

share as far as goods exports are concerned. This is not the case here.

|

| source: Eurostat |

A further takeaway from the chart above is that

the slowing down of growth in Greece’s export market share coincided with the

acceleration of growth in the respective shares of Bulgaria and Romania. Again,

correlation is not causation but…

Finally. let’s take a look at the services

balance. Here too the claim was that Greek services exports suffered due to

Euro’s strength. Well, I have a chart here that might tell a slightly different

story.

|

| source: Eurostat, own calculations |

As the EUR strengthened relative to the USD,

the balance improved and later in the decade, as the EUR weakened after 2009 it improved as well. Can

someone seriously believe that currency fluctuations are the only factor at

play here? International trade is such a multifaceted affair that very careful and

painstakingly-detailed analysis is required to get a whiff of the factors

leading to such changes. Besides, looking at balances does not always tell the

whole story since changes could be driven by the import-side or the

export-side.

Once again the post is

very long, so I'd better wrap this up. I think that changes in the Greek current account cannot be

attributed to the Euro’s strength/weakness. The widening of the deficit in the

00s is, always in my humble opinion, mostly a demand-driven affair. If one wants to dig further, deeper structural problems of the Greek economy will start to emerge (e.g. the composition and stationarity of the country's export basket or the miniscule external sector/lack of international orientation of the majority of businesses, etc.). Naturally,

some part of it can be attributed to loss of competitiveness but what part of

it is due to the emergence of new exporters and what due to currency-induced, reduced

price-competitiveness? This is my point exactly, claims that loss of

competitiveness can be blamed on currency strength alone border to the

simplistic…